An Update on All Things Offshore Energy Services

TotalEnergies Wins Mopane Bid, Borr x Noble Deal, Transocean Skyros Contract

Introduction

The world of offshore deepwater energy production is an inherently slow-moving process which often frustrates the investment community. If one takes the time to think of the process of deep-water oil discovery, it is unsurprising that cycles tend to be a slow grind in either direction. The average distance offshore for today’s deepwater basins are around 100 miles, add to that the need for an FPSO, a drillship and subsea infrastructure (SURF) and the timing of offshore capex from E&Ps balancing budgets, one can understand why these timelines can move out to the right.

From a supply and demand perspective today the ultra-deep water (UDW) vessels are roughly 5-7 vessels “loose” which will be remedied between now and 2027 as offshore development continues to ramp and vessels get contracted. While the cycle itself is slow moving, there has been a healthy amount of new information in the last few days that I think is worth addressing. The first is TotalEnergies 40% stake in Galp Energia (GALP) Mopane field in the Orange Basin. The second bit of news is sale of 6 Jack-up (shallow water) vessels from Noble including 5 to Borr Drilling. Finally, we will look at Transocean Skyros’s most recent contract that extends into 2027.

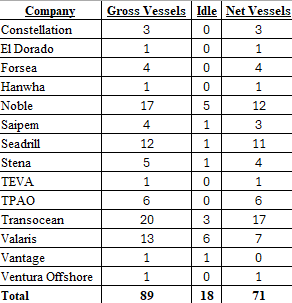

Below is our best estimate of the global UDW fleet by company to give you a sense of utilization in real time, and what needs to happen for the market to get “tight” we think the Total x Galp Energia development in Mopane will require no less than 2 drillships with potential for more. It is important to note here that TPAO is a Turkish owned entity that uses these vessels for state development. I bring this up because when we are thinking about the supply and demand dynamics and who is competing for contracts these vessels are sort of “off the market” for competition for 3rd party charters. Netting those vessels out we are looking at 83 gross vessels with 18 idle for a net active fleet of 65 when cleaning up for TPAO vessels leaving the market 8 vessels long.

When we are talking about being long 8 vessels it is important to note that our idle vessels are a combination of cold stacked, warm stacked, and vessels on contract awaiting work. Below you will notice Noble, Valaris, and Stena all have vessels that are contracted but waiting till 2026 to begin work. In addition, Vantage has an LOI out and is working to contract Platinum Explorer as well. If you clean up for these vessels and add them to contracted vessels by mid 2026 to early 2027 this is 7 additional vessels that will be added to the active fleet in 18-24 months. In that case our idle vessels drop to 11 and our net working fleet becomes 83 working vessels (89 - 6TPAO = 83 gross - 11 idle = 72 + 7 = 79) leaving 79 working vessels on 83 gross which excludes any additional work Venus, Mopane or Shells discoveries might require from drillships in which we estimate 2 at a minimum for Mopane.

TotalEnergies + Mopane