Borr Drilling Q2 Earnings

PEMEX Gets a Boost, 2026 Contract Coverage Concerns

Earnings Summary

Revenue: $267,700,000

Net Income: $35,100,000

2025 Utilization: 84%

Day Rate: $145,000

YTD Free Cash Flow: $106M

Commentary

It was nice to see Borr report positive figures for the quarter and show some signs of life. The stock has been absolutely hammered in recent history and for seemingly good reason. The business did not run for Chapter 11 protections and is heavily leveraged as a result. On top of far too much debt, all three of the businesses major markets have operational problems that effect Borr’s financial performance.

The Middle East is the largest market for shallow water drilling activity in the world and is suspending vessels and generally pushes to keep day rates in a stranglehold. While Borr is not contracted heavily in the Middle East, because the demand is so large their day rate levels will bleed into every market globally.

Another large market for Jack up demand is Norway who, along with the rest of Europe, continues to openly disparage its hydrocarbon producing industries and seeks to phase them out entirely with the North Sea being a basin of discussion.

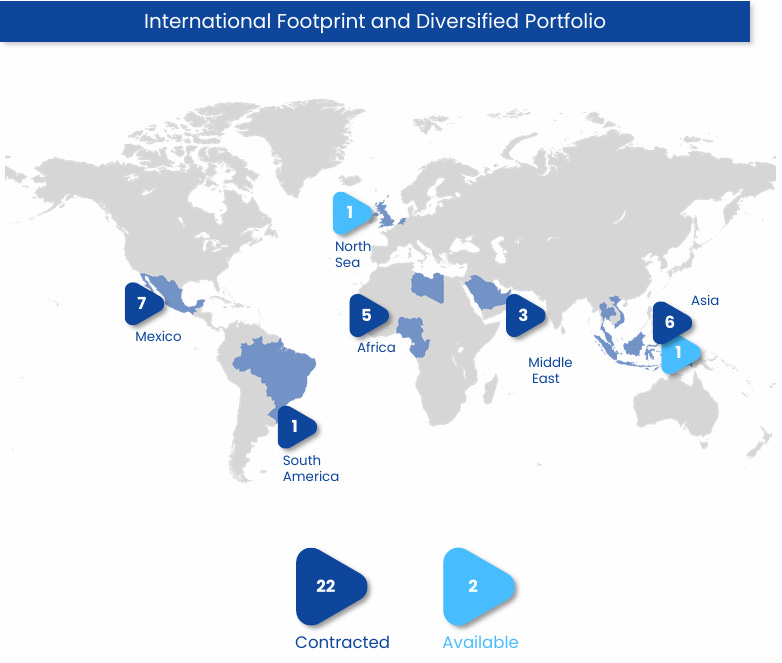

Finally, there is Mexico that is a large call on Jack up demand that can not afford to pay for offshore development with PEMEX suspending payments to its customers. Borr specifically had three vessels suspended in Mexico.

It appears that we have hit a near bottom in sentiment for Borr Drilling that has been reflected in its current valuations. With that said, we think the fears over Borr as a going concern are overblown, and that in the coming years they will be able to generate their current market capitalization in free cash flow in a 24-36 month period.

Balance Sheet